Revisiting the stablecoin trilemma: the current decline of decentralization

Words: Chilla

Compilation: Block unicorn

preface

It's not for nothing that stablecoins are in the spotlight. In addition to speculation, stablecoins are one of the few products in the cryptocurrency space that have a clear product-market fit (PMF). Today, the world is talking about the trillions of stablecoins that are expected to flood the traditional finance (TradFi) market over the next five years.

However, it's not necessarily gold that shines.

The initial stablecoin trilemma

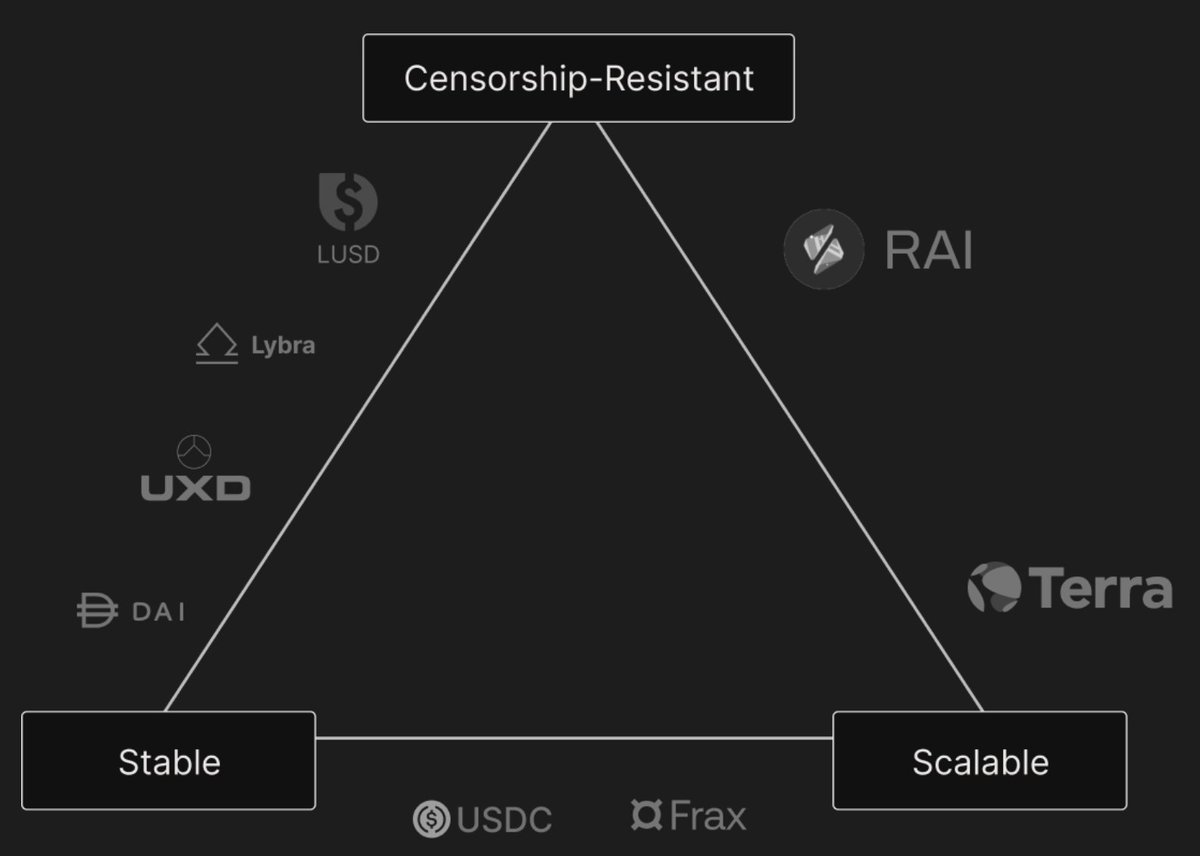

New projects often use charts to compare their positioning with their main competitors. What is striking but often downplayed is the recent regression of decentralization.

The market is developing and maturing. The need for scalability collides with the anarchic dreams of the past. But a balance should be found somehow.

Initially, the stablecoin trilemma was based on three key concepts:

-

Price stability: Stablecoins maintain a stable value (usually pegged to the U.S. dollar).

-

Decentralization: There is no single entity control, which brings censorship-resistant and trustless characteristics.

-

Capital efficiency: The peg can be maintained without excessive collateral.

However, after many controversial experiments, scalability remains a challenge. As a result, these concepts are constantly evolving to adapt to these challenges.

The image above is taken from one of the most important stablecoin projects in recent years. It deserves credit for its strategy of going beyond stablecoins and evolving into more products.

However, you can see that the price stability remains the same. Capital efficiency can be equated to scalability. But decentralization was changed to censorship-resistant.

Censorship resistance is a fundamental feature of cryptocurrency, but it's only a subcategory compared to the concept of decentralization. This is because the latest stablecoins (with the exception of Liquity and its forks, as well as a handful of other examples) have a certain centralization characteristic.

For example, even if these projects utilize decentralized exchanges (DEXs), there is still a team responsible for managing the strategy, seeking yields and redistributing them to holders, who are essentially like shareholders. In this case, scalability comes from the amount of earnings, not from the composability within DeFi.

True decentralization has been frustrated.

motivation

There are too many dreams and not enough reality. On Thursday, March 12, 2020, the entire market plummeted due to the pandemic, and what happened to DAI is well known. Since then, the reserves have mostly shifted to USDC, making it an alternative and somewhat acknowledging the failure of decentralization in the face of Circle and Tether's supremacy. At the same time, attempts at algorithmic stablecoins like UST, or rebase stablecoins like Ampleforth, have not yielded the desired results at all. After that, legislation further worsened the situation. At the same time, the rise of institutional stablecoins has weakened experimentation.

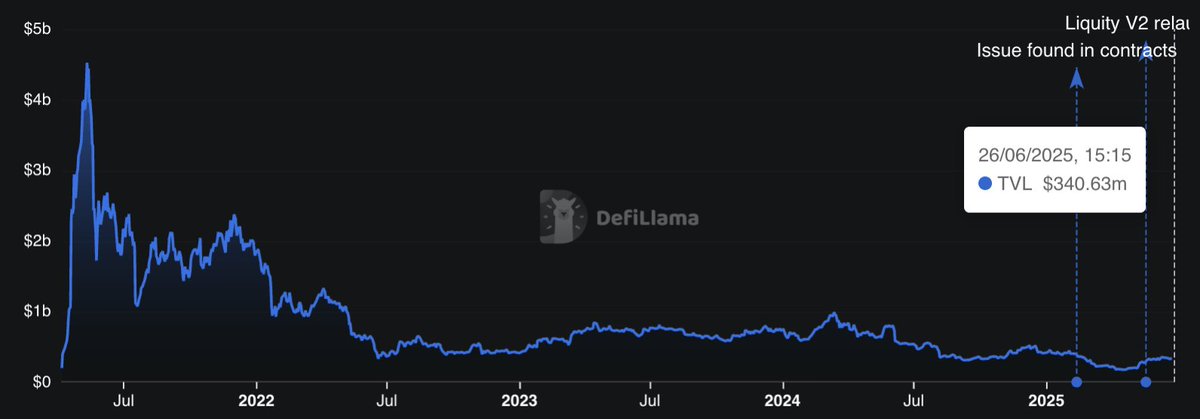

However, one of these attempts has achieved growth. Liquity stands out for its immutability of contracts and the use of Ethereum as collateral to drive pure decentralization. However, its scalability is lacking.

Now, they recently launched V2 with several upgrades to enhance pegged security and provide better interest rate flexibility when minting their new stablecoin, BOLD.

However, a number of factors have limited its growth. Compared to the more capital-efficient but yieldless USDT and USDC, its stablecoin has a loan-to-value (LTV) ratio of around 90%, which is not too high. In addition, direct competitors that offer intrinsic benefits, such as Ethena, Usual, and Resolv, also have 100% LTV.

However, the main problem may be the lack of a large-scale distribution model. Because it is still closely related to the early Ethereum community, there is less focus on use cases such as proliferation on DEXs. While the cyberpunk vibe is in line with the spirit of cryptocurrency, it could limit mainstream growth if it is not balanced with DeFi or retail adoption.

Despite the limited total value locked (TVL), Liquity is one of the projects whose fork holds the most TVL in cryptocurrency, with V1 and V2 totaling $370 million, which is fascinating.

The Genius Act

This should bring more stability and recognition to stablecoins in the US, but at the same time it only focuses on traditional, fiat-backed stablecoins issued by licensed and regulated entities.

Any decentralized, crypto-collateralized, or algorithmic stablecoins either fall into a regulatory gray area or are excluded.

Value proposition vs. distribution

Stablecoins are shovels used to dig gold mines. Some are hybrid, primarily institutional-oriented (e.g., BlackRock's BUIDL and World Liberty Financial's USD1) that aim to expand into traditional finance (TradFi); Others are from Web 2.0 (such as PayPal's PYUSD) and aim to expand their total addressable market (TOMA) by reaching out to native cryptocurrency users, but they face scalability issues due to a lack of experience in new areas.

Then, there are projects that focus primarily on underlying strategies, such as RWA (like Ondo's USDY and Usual's USDO), which aim to achieve sustainable returns based on real-world value (as long as interest rates remain high), and Delta-Neutral strategies (like Ethena's USDe and Resolv's USR), which focus on generating yield for holders.

All of these projects have one thing in common, albeit to varying degrees, and that is centralization.

Even decentralized finance (DeFi)-focused projects, such as the Delta-Neutral strategy, are managed by in-house teams. While they may leverage Ethereum in the background, the overall management is still centralized. Actually, these projects should theoretically be classified as derivatives rather than stablecoins, but this is a topic I've discussed before.

Emerging ecosystems such as MegaETH and HyperEVM also offer new hope.

CapMoney, for example, will adopt a centralized decision-making mechanism in the first few months, with the goal of progressively becoming decentralized through the economic security provided by the Eigen Layer. In addition, there are Liquity's fork projects such as Felix Protocol, which is experiencing significant growth and establishing itself among the chain's native stablecoins.

These projects have chosen to focus on emerging blockchain-centric distribution models and take advantage of the "novelty effect".

conclusion

Centralization is not a negative in itself. For projects, it is simpler, more controllable, more scalable, and more adaptable to legislation.

However, this is not in line with the original spirit of cryptocurrency. What guarantees that a stablecoin is truly censorship-resistant? Is it not just a dollar on the chain, but a real user asset? No centralized stablecoin can make such a promise.

So, while the emerging alternatives are attractive, we shouldn't forget the original stablecoin trilemma:

-

Price stability

-

Decentralization

-

Capital efficiency